The global economy is driving toward authoritarianism, but Bitcoin offers autonomous, decentralization that can save the average investor.

Part I: Bitcoin As A Tree, Persistence And Deep Structures

A Reverie

Perhaps if I had been more brazen, the title to part one of this series would have ended up as something more tantalizing, something punchy like “Bitcoin Is A Palm Tree, And Fiat Is A Coconut.” But for better or worse, such a title felt saturated with a bit too much levity, too tropical and trivial for such a weighty topic.

In truth though, the palm tree imagery would have actually been a very accurate allegory of how the bitcoin and fiat roadmap will evolve as we progress further into the 21st century. A royal palm, roystonea oleracea, bobbing feverishly in a torrential squall, though never ceasing to retain a firm grasp to its roots deep under the soil. And as with any storm, the only Darwinian necessity for this tree is one of survival, to ride out the tempest as unscathed as possible.

Other trees and structures may shatter and snap in capitulation to the harsh vagaries of nature, leaving more sunlight for our royal palm to absorb once the sky has cleared. The debris from all that had not been robust enough to survive the attack, metabolized by colonies of termites and brush fires, transformed into lush and fertile soil. A new base layer from which to rebuild and thrive. An apt metaphor, in light of the fact that soil happens to be the only physical medium ever observed in nature capable of transforming death into life. Likewise, an absolutely scarce, incorruptible sound money is the only economic medium capable of breathing economic life into a decaying and debased financial system.

A Warning

“Harmlessly passing your time in the grassland away

Only dimly aware of a certain unease in the air

You better watch out

There may be dogs about

I've looked over Jordan, and I have seen

Things are not what they seem

What do you get for pretending the danger's not real

Meek and obedient, you follow the leader

Down well-trodden corridors into the valley of steel

What a surprise!

A look of terminal shock in your eyes

Now things are really what they seem

No, this is no bad dream”

-Roger Waters, “Sheep,” 1977

A Prophecy

“Did you hear about the rose that grew from a crack in the concrete?

Proving nature's laws wrong, it learned to walk without having feet.

Funny, it seems to by keeping its dreams, it learned to breathe fresh air.

Long live the rose that grew from concrete when no one else even cared.”

–Tupac Shakur, “The Rose That Grew from Concrete,” 1999

Before we can fully appreciate the persistency characteristic of bitcoin inferenced above, it is perhaps helpful to contextualize how and why such “antifragility” (something we will define in greater detail further below) will inevitably reveal itself like a crack of thunder, a slap in the face, allowing us all to witness its deeply undervalued utility.

To accomplish this, let us take a slight detour using a modified version of the Socratic questioning technique.

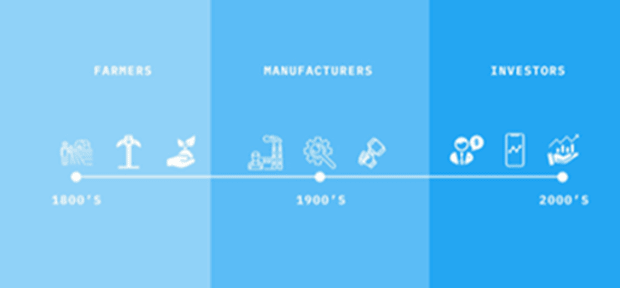

A Theory: The Stampede Of The Mass Investor Class

Esteemed polymath tech investor Balaji Srinivasan, in his conceptual model of a decentralized pseudonymous economy, controversially has declared:

“In the 1800s, everybody was a farmer. In the 1900s, everybody was in manufacturing. In the 2000s, everybody becomes an investor… And one of the things that people don't understand until they're an investor is this idea that money is abundant.”

-Balaji Srinivasan, “Invest Like the Best Podcast With Patrick O’Shaughnessy”

A Discussion

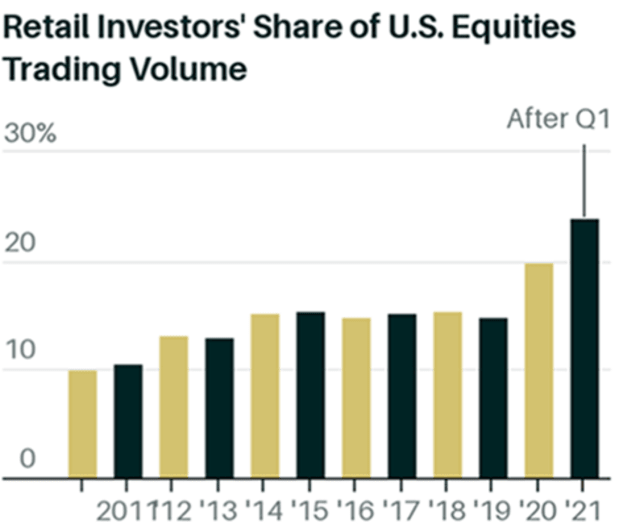

Let us take the above statement at face value and accept it for the moment as an evolving a priori reality. I think most of us would agree that such a broadening in reach of the investor class is indeed undergoing rapidly escalating momentum, particularly accelerating in the post-pandemic world. It is hard to deny the hard evidence (discussed below), as well as the observed cultural spotlight that has emphasized self-directed stock market investing. The evidence is everywhere, even scrolling across my newsfeed as I wrote this essay:

“Robinhood Working on Feature to Let Users Invest Spare Change”

“Investing spare change has become an increasingly popular strategy for new stock traders, and is a key piece of competing apps such as Acorns, Chime and Wealthsimple.”

With Robinhood’s symbolic IPO now etched into our recent memory, headlines as stated above are perfect examples for our discussion. Micro-funded stock market investing would epitomize this evolution towards a mass investor class. I, for one, see this change all around me, in my professional life in the hedge fund industry, in a culture of growing FOMO, greed, and anxiety, all the way to my personal interactions with friends and family and on social media. I even believe this is what many policymakers and technocrats are consciously aspiring to incentivize. And it disturbs me.

What are the implications of such a societal transformation? And what are its root causes?

Such open-ended questions arising from this observation are one reason why I am so attracted and intrigued by Srinivasan’s conjecture in the first place. His statement opens the door to a variety of discussions and touches on some very important themes.

Some of these themes pertaining to the inevitability of a decentralized economy are topics that will be discussed in greater detail in part two of this series. In the meantime, let us set the stage by understanding why a mass investor class is being encouraged, how it will lead to even more centralization, and how all of these opened doors are one way escalators, guaranteed to lead to further path dependent decisions trees, and eventually generate near infinite instability and systemic frailty.

And what will become overwhelmingly clear will be the holistic interplay between the inevitability and unsustainability of this path on one side of the coin. And then bitcoin’s persistence on the other side, patiently waiting for its turn to be hoisted into the air, spinning frenetically, though calm and collected as it patiently anticipates a face-up landing.

A Sandwich Metaphor

What Srinivasan’s prophecy unknowingly exposes is the reality of a dangerous transitional period in which the global economy currently finds itself. We are situated in a confused state of limbo right now, sandwiched precariously between decentralization and centralization.

The cultural energy of this fluid temporal state certainly solicits a certain “unease in the air,” though the growing discontent is palpable. And just as the events of the COVID-19 pandemic have propelled the intensification of many trends, one of these trends is indeed a manifestation of a “proletariat” and aggressively-expanding investor class. And while such a progression has many positive attributes — ranging from self empowerment, the opportunity for new wealth creation in the short run, and financial education about markets, risk management, money, and economic theory — all such benefits are sadly misguided and short-sighted. In the end, these very tangible benefits are destined to be diluted and vanquished by ominous forces.

The main reasons as to why a commoditization of the investor class is such a dangerous evolution can be primarily attributed to timing, historical context, and the implications of what this mass investor society will require in the form of second and third derivative effects.

Please be patient below, for this first section is unavoidably heavy with some financial data and terminology. However, such data is imperative to help us understand the bigger picture of what is going on and will pay dividends further into the article and series as we expand on the bigger ideas of our thesis.

I am not a doomsayer. I do not live in a bunker. I have seen too many investors fall victim to overly bearish narratives, missing out on great asset inflations that such negativity obfuscated. The purpose of this essay, however, is not to lay out some near-term investment thesis. That said, what I have begun to witness with increasing clarity as an investor, as a member of our society who cares about the world my children inherit, is growing evidence of an unavoidable trap. A trap with only one realistic solution. So, the financial data herein is merely a tool, a language to help us see this insight. In fact, the main message of this series is much less about finance and markets, and much more about human nature, history, and the impact incentives and ideological conflict will have on the outcome of the bulk of this century.

So, bear with me as I take us further down this rabbit hole of fated blocks in our chain of reactions.

Block One: Historical Context Matters. It Turns Out That Timing Is Everything

A mass investor class, driven by false premise and perverse incentives, is ironically forming after a period unparalleled historic asset inflation.

We have just witnessed an unprecedented 40-plus years of financial asset inflation, debt accumulation, de-regulation, and monetary opulence. An epic bond bull market where the risk-free rate has gone from 16% to nearly zero, the stock market relative to our productive capacity is at record (see below chart), almost all valuation metrics are at historical highs, and irrational behavior has expanded dramatically (exemplified by SPACs, r/WallStreetBets, meme stocks, retail margin debt, and of course many pockets of the “crypto” universe).

At the same time, government and corporate leverage are also both at extremes. These statistics become even more excessive once accounting for off-balance-sheet government liabilities such as social security, medicare, pension obligations and off-balance-sheet defense budgets. This is in addition to factoring in rosy corporate guidance assumptions and lots of company management teams getting desperately creative with earnings add-backs tricks, and aggressive accounting engineering strategies. Said differently, the individual investor is professionalizing at the end of one of the biggest, most Homeric blow-out parties of all time. Forgive the cliched baseball metaphor, but this is like a player being called up from the minor leagues right before the off-season, after a seven-game dramatic World Series finale.

Is this really a good development for society? This is actually rather typical of the behavior observed and participation that occurs in peak periods of bull markets. However, there are a few key differences here relative to the typical bubble burst.

First, we are referring to such behavior in the context of these investments being made under the guise of newfound professionalism and empowered career shifts. There is a sense of entitlement to riches, and an expectation from both policy makers and new investors alike that it is their right to attain wealth from capital markets, and to do so with very little embedded risks. Further, as evidenced by a declining labor participation rate, a society of investors creates double risk. As more people forgo other modes of labor, we become a society of “renters” rather than “doers.” We reverse the arrow of history that has always led to increased specialization and division of labor. So, not only are more individuals now exposed to financial assets than ever before, but this expanding cohort has done so at the opportunity cost of foregone employment and earned wages elsewhere.

The stakes are higher, and the margin for error lower. And such behavior is actually being endorsed both culturally, as a means of revolting against the wealthy class, and politically, as a liberal entitlement for asset ownership to see greater distribution, without any regard to the underlying value and risk of such assets. This is different than a simple transitory financial bubble. This is a hot air balloon floating up through the stratosphere, never to feel the earth’s firm embrace again.

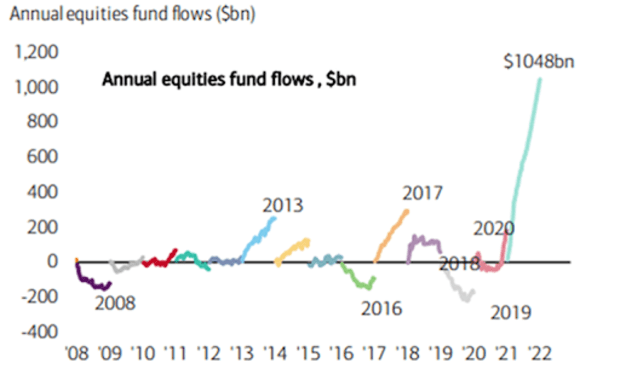

Mass investor class adoption is accelerating.

The annualized rate of equity inflows thus far for 2021 are about $1 trillion. For some perspective, this is greater than the total cumulative inflow into equities over the entirety of the last 20 years!

The above chart illustrates $1 trillion annualized inflow into stocks in 2021, compared to $800 billion cumulative equity inflows from 2001 to 2020. Let that sink in for a minute before continuing this essay. We see so many insane and unprecedented charts, memes, and statistics these days, that it is easy to gloss over this graph. But this really says something profoundly troubling about where things are heading.

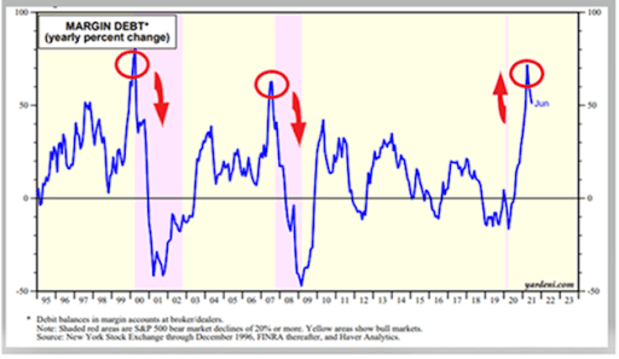

Margin debt for leveraged equity trading, tracked by the Financial Industry Regulatory Authority (FINRA), has historically been a signpost of individual (or “retail”) investor excitement and greed within the equity markets.

The below chart plots the annual percentage rate of increase in margin debt, which historically has anticipated recessions, marked by the purple-shaded regions. However, we can see in the recent period, margin has spiked at a historically-unparalleled pace, perhaps peaking in the near term.

But the key observation here is that this rapid rise has occurred after that purple bar, rather than before it. Margin debt did not precede a crisis but was the response to it. We saw hints of this in 2009, but that was after a massive purging of bank and housing leverage, and a large write down of asset values. The COVID-19 crisis did not allow for such a purge, and instituted policies to reinvigorate retail equity investment dramatically. This is new behavior.

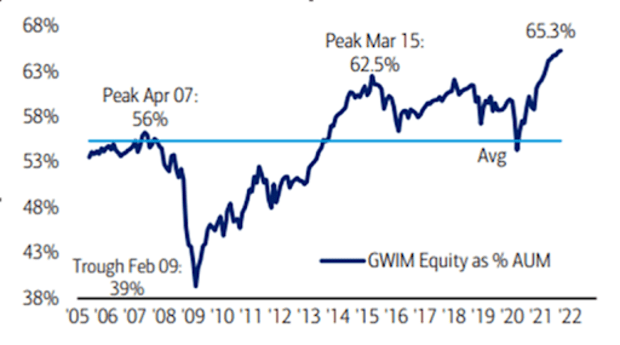

Bank of America (BofA) Wealth Management clients’ equity allocation are at all-time highs.

What this last chart directly above demonstrates is that individuals in the U.S. are no longer building savings from excess income, but from asset inflation. Definitionally risky and inflation-sensitive financial assets are now the primary stores of value for most households that can afford to own them.

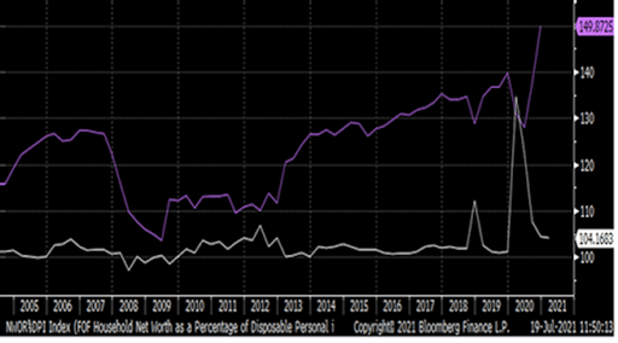

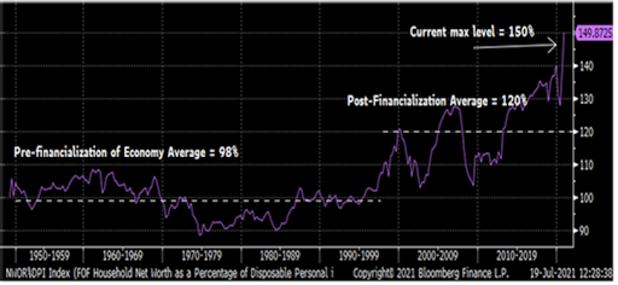

For a greater historical context, below is the same household net worth as a percentage of disposable personal income, going back to 1945.

The Death If Creative Destruction

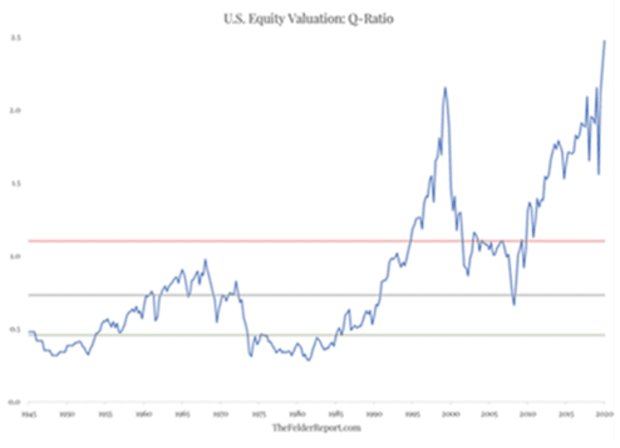

Below is a graph of an indicator known as Tobin’s Quotient, also known as the “Q ratio.” In essence, it is the ratio of the stock market’s current capitalization, divided by the real-world replacement cost of the assets associated with that equity.

As visualized in the below chart, this ratio is at historically unprecedented levels. The chart ranges from post-WWII to present and expresses that equity valuations are currently nearly two-and-a-half times their replacement value. This compares to a 75-year average ratio closer to the replacement value.

Admittedly, this analysis is not free of nuance, as our economy has shifted into an information age characterized more by digital economies, whereby assets become more intangible and therefore it becomes harder to value replacement costs such as intellectual property and the goodwill of network effects. But even if we account for this change, the current Q ratio still stands at over three times the replacement value, compared to the 1990s pre-dot-com bust era of a 1.4-times replacement value average, and a post-dot.com bust era average of closer to 2.3-times the replacement value.

No matter how you slice the data, what this demonstrates is the sheer extent of companies financially valued in a manner completely dislocated from their economic reality. So-called “zombie” companies that should not exist in a truly free market, often carrying high quantities of unproductive debt to sustain themselves, thrive in such a brave new world. These entities trap good money and keep it petrified within decaying structures. As a professional investor who spends a great deal of time investing in high-yield corporate credit, I see this insanity on a daily basis.

At some point, the only way to reconcile such imbalances is either by way of mass restructurings, bankruptcies, and debt defaults, or through inflation. Inflation acts to boost the denominator of replacement value, in an alchemist’s potion of superficial rectitude. Inflation, as witnessed throughout human history, is by far the more palatable solution for economists, Wall Street investors, and of course politicians who have two-to-four-year outlooks on the world.

But the irony of this fact is that such a realization is to also explain how we got here in the first place.

The Denial Of Quality

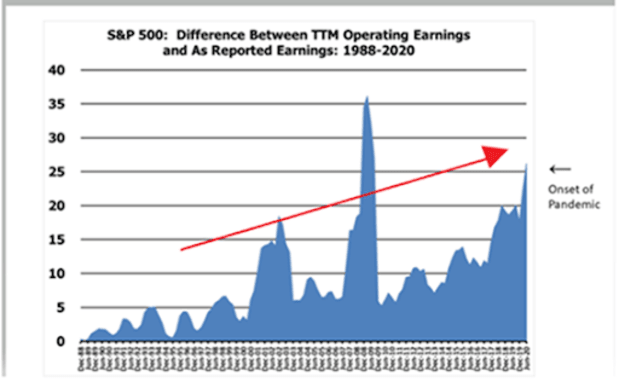

Below, we can observe more evidence of declining quality. In this instance, we are not referring just to the collapse of creative destruction and balance sheet quality, but to the quality of overall corporate earnings themselves.

The very metrics we trust to help us ascertain the complex world of data around us have been gamed and manipulated to a point where the measure has become the target. GAAP, or “generally accepted accounting principles,” is an accounting protocol designed to limit the debasement of earnings through opaque, arbitrary and misleading add-backs. Sometimes, there are indeed valid non-GAAP adjustments that need to be made to get an accurate picture of a company’s true run rate earnings potential. On the whole, however, such “non-GAAP” adjustments to GAAP reporting has tended to produce a picture of lower integrity and confidence.

Despite this, we have become so accustomed to such adjustments that market participants and regulators have accepted the gradual deviation unblinkingly. It is perhaps not surprising that non-GAAP adjustments first became “rooted into the fabric of financial reporting” in 1988, when many policies of financialization of the economy accelerated. It is also worth mentioning that most stock-based compensation expense is added back to non-GAAP earnings. So, there is a self-referential dynamic at play here, as non-GAAP earnings boost the appearance of profits, helping to inflate stock valuations, which in turn inflate the very stock-based compensation that is helping inflate the earnings in the first place!

The below chart plots the spread of non-GAAP earnings minus GAAP earnings:

This spread tends to spike in recessions as non-operating losses accrue. But interestingly, in years beyond the recession, the trend resumes its path toward weaker quality.

Block Two: A Hot Air Balloon

The result of this situation is that system fragility balloons rapidly, necessitating a deterministic path dependency of increased data manipulation, government support, regulation, and free market intervention.

Such a historical valuation and asset performance context as articulated above means that broadening financial asset exposure to a more diverse and larger population creates unacceptable systemic risk for the economy over the long run. To borrow a game theory phrase, the stock market becomes a single point of failure.

As I’ve laid out in a previous article, “Thinking Too Small And The Pitfalls Of The Inflation Narrative,” it also becomes a means of insidious money printing via financial asset creation, rather than by the more obvious money supply expansion of our parents’ and grandparents’ generations. This incentive to inflate by decree of moral hazard — or implicitly-guaranteed financial asset inflation — is even easier to accomplish when technology is making more and more products and services cheaper or outright costless, and when supply constraints like we are experiencing now make the consumption of physical “stuff” less desirable or even impossible in some cases.

Properly-priced debt markets create return hurdles to investment that incentivize only those endeavors that can create new productive capital. Overly-cheap debt incentivizes leveraging of the existing capital stock, without a need or desire for any productive gains. And even when new capital investments are eventually made, the clear incentive is to do so with that cheap financing, rather than from savings and cash flow. This eventually leads even productive capital allocators down paths of excessive leverage.

Meanwhile, as assets inflate, the only way to maintain the desired standard of living involves moving any savings instead into riskier financial assets like stocks, bonds and real estate. This is because the return on investment for new capital formation always takes longer to play out relative to re-harvesting the existing capital stock when inflation is all but assured by systemic moral hazard. Add to this the fact that oppressed and manipulated interest rates are pilfering from the very future for which new capital would be invested (discussed more below). This further disincentivizes any material investment in new capital stock.

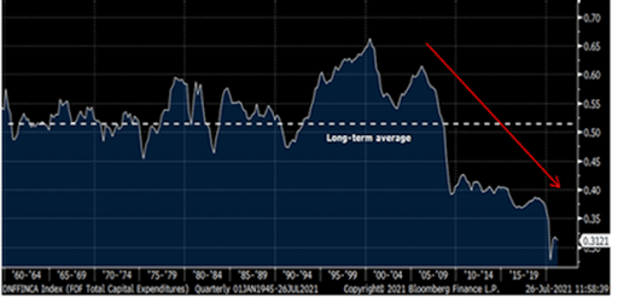

The below chart plots a ratio of total U.S. capital expenditures in nominal dollars, divided by the denominator of base money put into the system, measured by M2 money supply. Ever since peaking into the dot-com crisis, investment in new capital formation has plummeted relative to new money creation. This begs the rhetorical question as to where all of the excess new money is flowing, if not to new capital formation. The answer is financial assets, of course.

Thus, the incentives are as clear as a stiff slug of Stoli. And, for most of the past 30 years, only the wealthy have been part of this game design, gaining a seat at the table with their existing assets, their “proof of stake.”

However, it is becoming more evident that ubiquitous moral hazard, further time preference shrinkage, and freshly-minted savings are the most efficient next stage in this decision-tree of false free will. Policy makers on both sides of the aisle have incentives to embrace such a narrative. They will aim to drive middle-class net worth as opposed to the old playbook relating to the improvement of middle-class income, education, social safety nets, and tax redistribution. Meanwhile, the right side will gladly pass their baton from trickle-down supply-side monetarist economics, with its self-deluded “hopium” that the American corporatocracy will share the wealth, and likewise embrace financial inflation and socialized capitalism. The right will perceive such centralization of capital markets as distasteful, but better than an alternative of Keynesian socialism and redistribution. Both sides will trade their core principles for a solution that actually delivers results, albeit at a tremendous cost.

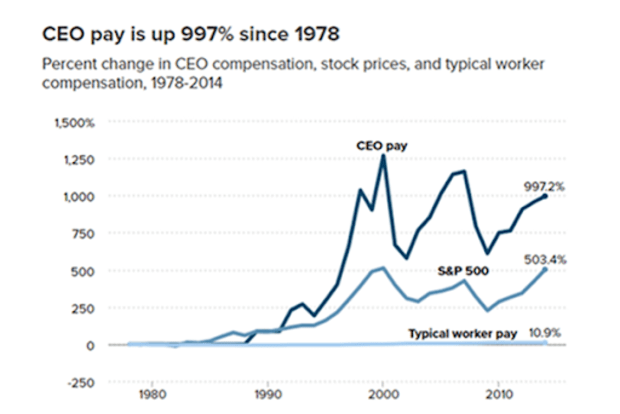

If you were a policy maker looking at the below chart, what would be the least risky and most obvious mechanism to rectify such immense divergence? Easy: Simply tie “typical worker pay” to the S&P 500, and boom! Mission accomplished!

Ok. So, let us assume we’ve now got the ball rolling and are indeed starting to tie worker compensation to the stock market through various means. But how is such a feat accomplished? It’s not as though the government can force employers to pay wages in the form of stock market indices.

Well, not directly. The answer lies in a blended recipe of altered incentives. Moral hazard and implicit backstop of equity prices as described above is certainly the epicenter of such a strategy.

But there are endless others: Fiscally-induced higher individual savings with incentives to invest any excess savings; de-globalization efforts that encourage U.S. citizens to invest and save more domestically rather than consumer imports from China; and the natural progression of technology and financial innovation simply “doing their thing,” creating greater on-ramps for democratized investing — examples of this would be products such as exchange-traded funds (ETFs), trading platforms like Robin Hood that simplify the user experience, social media-powered blogs, YouTube channels and alternative infotainment platforms that build confidence and then sprinkle this broth with a hefty dose of FOMO at the cultural level. Another obvious mechanism would be through higher income taxes to divert money toward financial investment, and greater capital gains taxes to incentivize stock market HODLing behavior. These are just examples. The point here is that there is a limitless toolbox available to further such goals, both intentionally as well as organically by way of the system’s natural incentives.

“But wait,” you say. “What is wrong with a higher savings rate and less consumption? After all, is this not a core principle of many Bitcoiners?”

The problem is that even prior to such a societal career shift as we are witnessing today, the level of asset prices relative to their fundamental value had already crossed a point of no return, creating a frustrating sense of fatalism for many open-eyed market participants.

Decades of declining discount rates have stolen so much value from the future already that there are no future growth seedlings left to even take root. So, the problem here is not saving in and of itself, but the specific savings pastures into which individuals are being herded. Saving is not saving if it is not being funneled into real stores of value. Just the opposite in fact. The only way to maintain current standards of living requires perpetual asset price rates of growth, which in turn necessitate more and more debt.

If the government and normative cultural influencers were to export such a dynamic to the masses, what should we expect the outcome to be? Is it utopian equality and abundance? Or is it central planning, a marginalized free market, and socialized economic activity? You guessed it! Door number two, Bob!

Block Three: Math

One of the most influential variables that historically has been associated with the end of periods of great stability and strength has been wealth inequality. While such skewness is rarely the origin of a systemic collapse, it is almost always a symptom of the decay, and just as often plays a role in catalyzing the tipping point into decline. From the Mayans to the Roman Empire to the Chinese Three Kingdoms to the Ottomans to the French, Russian and Chinese revolutions, wealth inequality has always played a major role.

This is a big problem for the mass investor class strategy. This is because a goal of wealth redistribution with a strategy centered around asset inflation is statistically impossible to achieve.

Many proponents of this new investor class take the “fight fire with fire” approach. Yes, asset inflation — driven by modern monetary policy — has been the prevailing impulse of inequality over the last several decades. Why should the average individual not be able to get their just desserts as well? Ethically speaking, I take no issue with such retribution to some degree.

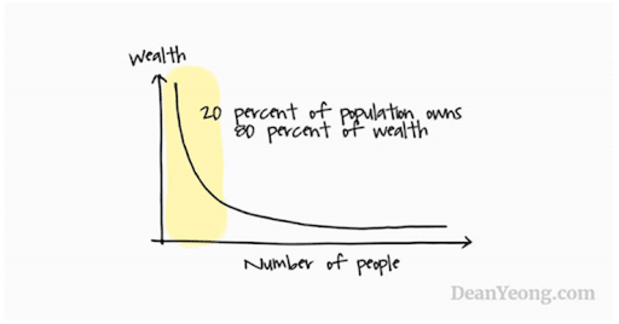

Unfortunately, it’s an illusion. The presiding growth curve that has been empirically witnessed as it pertains to wealth distribution has been found in the Pareto principle, a probability distribution whereby a small percentage of the sample group acquires most of the attainable value. Facets of this law, more colloquially known as the “80/20 rule,” are observed not just in wealth distribution, but prolifically throughout much of nature and human social environments.

We have experienced at least a half-century of Cantillon effects that have supported asset owners in exponentially outperforming relative to income owners. Even if we disposed entirely of such Cantillon effects and allowed the broader population equal access to financial assets going forward, and even if financial assets continued to generate historically anomalous returns, the “80 percenters” would never catch up. The reason for this is simply due to the nature of exponential growth curves as seen in the Pareto principle. Inequality would be maintained at the very least, if not continue its asymptotic expansion.

Pareto’s law: How asset inflation becomes a highly entropic state for wealth distribution, regardless of policy.

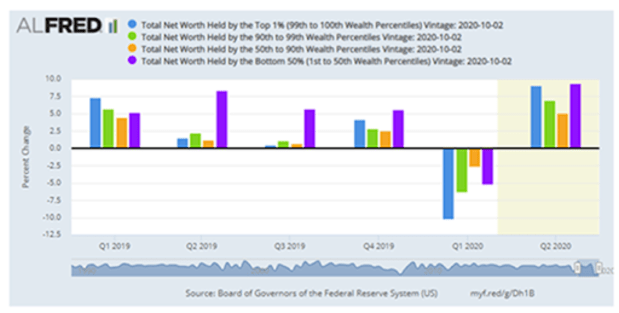

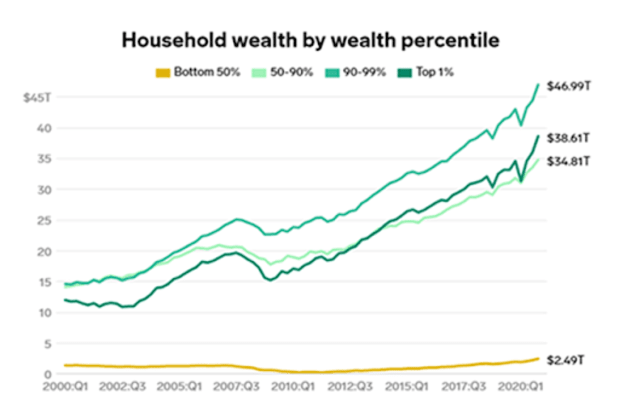

This Pareto probability distribution is exemplified quite dramatically after looking at 2020 as an outlier year, whereby the least wealthy percentiles actually saw the largest percentage improvement in wealth. However, while this is a lovely-sounding statistic for social media hype and political propaganda, it is purely a mathematical outlier caused by starting from such a low base and from such a low level of prior financial asset ownership.

Unfortunately, the banner year for the bottom 50% (purple bar below), did next to nothing to narrow the wealth gap from the top percentiles, as evidenced by the below chart.

2020 did nothing to rectify the problems of inequality. In fact, inequality only got worse. Why would a continuation of asset inflation look any different in the future?

If inequality cannot be corrected by the only policy tools available, the risks for social instability will only rise further. Ironically, when stability is threatened, this tends to only increase levels of centralization.

Have you ever been driving your car on a wet, slippery road, only to fish-tale unexpectedly? While our instinctual response would be to tense up and violently steer the wheel in the opposite direction to regain control, such a reaction would only worsen our dire predicament. One must steer into the chaos. Once control has gone, such a fate must be embraced, not opposed. This is the only way out. Further attempts at control only make matters worse.

Block Four: All Roads Lead To One Road, More Centralization

Once the inevitability of blocks one, two and three as stated above are appreciated, the path dependency of block four in our chain becomes absurdly apparent: Subsidizing asset prices through monetary debasement becomes the oblique way that society yields to ideologies like universal basic income (UBI).

UBI may end up in the very long run as explicit social welfare programs, or “helicopter money.” Of course, during COVID-19, we saw some discreet examples of this, turning something merely theoretical into a tangible part of the societal zeitgeist. However, it is a mistake to assume a linear path, that such policy will now settle as the initial and most effective vector for such policy going forward.

A more frictionless pathway would be the mechanism outlined above, whereby social welfare can be extolled circuitously. The brilliance of such a policy approach is that it would not require any incremental pieces of legislation, and no constitutional alterations to property rights. There are no foundational legal constraints. This implies that our current institutions have the power to accomplish such social welfare goals today.

One could argue that some changes would certainly make these aims easier to administer, like augmenting the Federal Reserve Act of 1913 and expanding the powers of the U.S. Treasury Department. However, the key point here is that such change is not required. If the reader finds this too far fetched, I would recommend listening to the taped conversations between ex-President Richard Nixon, and then-Federal Reserve Chairman Arthur Burns. It has happened before in this country, and in less dire circumstances.

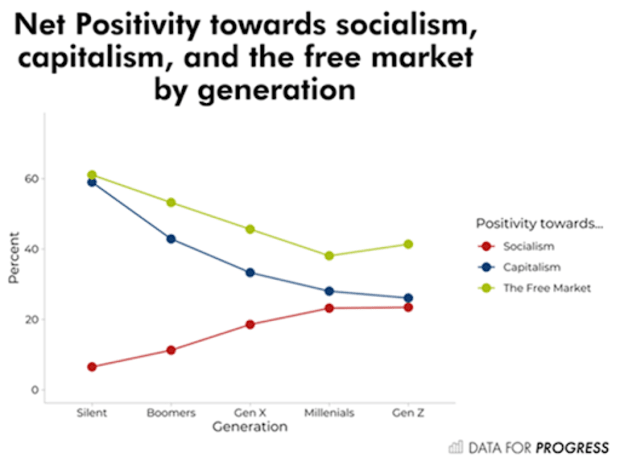

UBI advocates are here, and they have their own network effects:

American openness toward socialism, and a commensurate disdain for capitalist ideals, has increased dramatically over the last four generations. This has been well documented with recent generations, particularly millennials, but it is important to recall that such a trend has been consistent well before that, even with the boomer generation relative to their parents and grandparents.

This is rather alarming when one considers that this generation has been the biggest beneficiary of financial asset prices (coincident with the full embrace of the fiat monetary system) of any generation in American history.

A Quick, “Passifict” Detour: Passive Investing Socializes Capitalism

Bitcoin may be humanity's historically most perfect manifestation of a pacifist revolution, but passive investing is also a revolution, only with completely opposite implications.

Historical analogues are always dangerous, and each generational crossroads exhibit unique characteristics that can change the entire spectrum of outcomes. However, as a reference point, current trends reverberate with echoes of previous centralizing efforts designed to redirect our collective future and shift the public behavior, reminiscent of Franklin D. Roosevelt’s “new deal,” as well as Nixon’s “great society,” or even going back to German Chancellor Bismarck and his social welfare policies in the 1880s, which greatly enhanced the Second Reich’s military capacity.

Passive or indexed investing vehicles such as exchange-traded funds (ETFs) are yet another example of this shift toward a “mass investor class.” While such a trend may seem innocuous, it is cultivating the seeds of enormous societal change.

As discussed by Inigo Fraser-Jenkins, a highly-regarded maverick quantitative equity strategist at Wall Street firm Bernstein, passive investing can be compared to Marxism. This may sound hyperbolic, but unfortunately, I believe he is on to something important here, the point being that the democratization of capital markets by way of ETF proliferation and other passive investing products inadvertently leads to a socialization of capital.

It would all but complete our societal transgression from liberal democracy to social democracy, a trend that has been gradually underway, but accelerating over the past 75 years. Fraser-Jenkins compared passive investing to other societal externalities like the tragedy of the commons, whereby behavior that may be optimal for the individual investor can be quite negative for the aggregate society when all actors behave the same way (we will return to the problem of the commons later).

The unfettered expansion of passive investing does not look likely to subside any time soon. This is especially obvious when one simply looks at the below chart, or even at the hiring behavior on Capitol Hill, like the large representation of Blackrock alumni acquiring key roles in the current White House administration. Blackrock is the number-one manufacturer of passive investment vehicles in the world, with over $1.8 trillion in assets under management (followed by Vanguard in second place at $1.2 trillion).

Additionally, ESG and clean energy investment mandates further this shift, creating new products to bundle into thematic passive investment securities. Such bundles make it easier for ESG-approved companies to redirect capital away from those companies that do not fit the homogenous definitions prescribed. To be clear, there is nothing intrinsically bad about incentivizing cleaner energy and more sustainable economic practices. Of course, this is a good thing! However, when rules for such behavior become formalized, complex, and sometimes arbitrary and naively general, they impinge upon the competitive dynamics of free markets that would accomplish such goals more effectively.

Instead, such rules generalize the flow of investment, compensating those market participants best suited to game such a system. The new game defines the winners as those best able to adhere to the appropriate definitions as a means of acquiring low-cost capital. In a road paved with good intentions, we potentially end up in hell, robbing free markets of innovation, nuance, and differentiation. We write new rules of the game, rules that thoughtlessly increase centralization.

Mike Green, a distinguished researcher of passive investment stated back in 2020:

“Of managed assets, [passive investment] is now greater than 50% [and over 40% of total market capitalization]. That split though, is not uniform across demographics. Millennials are almost 95% passive. Boomers are only 20% passive. For the vast majority of millennials, their only exposure to the market… We make a lot of hype about things like Robin Hood and stuff, but the actual assets are tiny. The vast majority of the money that they’re getting is actually just going into things like Vanguard target-date funds.”

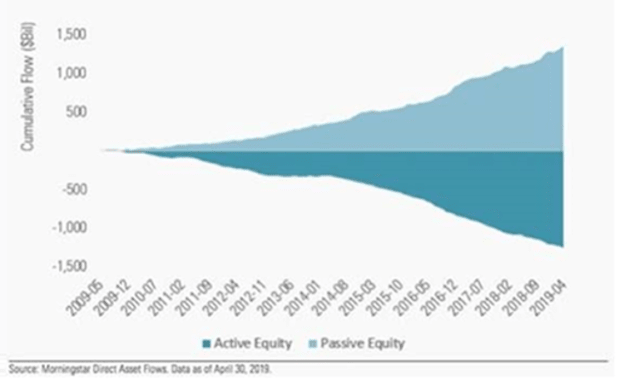

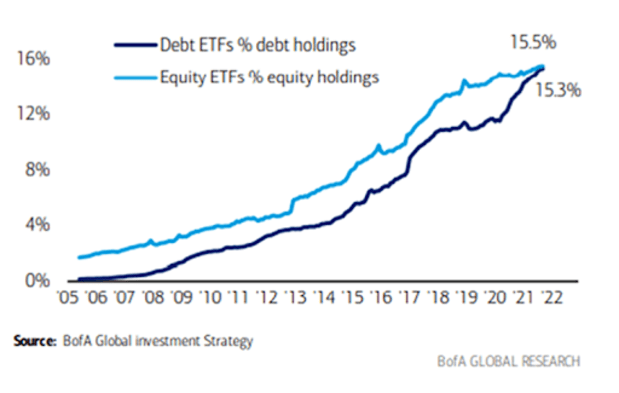

Active equity managers have seen outflows every year and passive investment vehicles have seen inflows every single year since 2006. And this trend is only accelerating:

Bank of America’s private client ETF holdings as percentage of assets under management (AUM). A hard trend to fight:

The passive singularity: Millennials have 95% of their retirement savings invested in passive vehicles. What is the logical conclusion of this freight train?

“One of the challenges that gets created as passive becomes a larger and larger share is that there becomes no discretion. There is no consideration of should the incremental dollar go in in the exact same fashion, right? That passive player has no instruction to sell. You exhibit increased inelasticity in terms of each incremental dollar that goes in. Imagine a scenario in which 100% of the owners of a company were passive and you tried to buy a share. There is no price at which they would be willing to sell to you unless they received an instruction from their end investors saying to sell shares to you. Prices could theoretically become infinite on that type of dynamic. Eventually, you would expect somebody to respond by saying, ‘All right, I will sell an additional share to you.’ Traditionally, that’s been accomplished by price-sensitive or return-sensitive discretionary managers who say, “Okay, this price is unwarranted by the fundamentals. Therefore, I’m willing to sell some of these shares to this person who’s expressing, in my view, an irrational demand for these shares.” If that demand is so strong and it gets absolutely extreme, people can synthetically create shares by shorting, but that is incredibly dangerous to do, an environment in which stocks are exhibiting this reduced elasticity.” –Green

The mass investor class faces a big incentive problem: What does the internet, digital property, and a tragedy of the commons have in common? Our retirement accounts.

The dismantled connection of choice from the capital allocation process brought about by passive investment proliferation has implications beyond the clear destruction of price signals. This is no small statement. A destruction of price signaling is as destructive as things can get for a capitalist system. Prices are the main form of communication we use in society to make appropriate economic decisions and choices. Its dissolution is of existential importance.

However, there are other problems to consider from this evolution of behavior as well. Ever since the runup to the 2016 U.S. presidential election, and at an accelerating pace since the onset of the COVID-19 pandemic, society has become more aware of the vast concentration of power that the internet giants and social media platforms carry.

Pockets of government and pockets of new and growing cultural progressive movements have quite easily influenced and incentivized these platforms to actively censor speech in our democracy. This is not a political statement, and this is not a judgement about the people being censored, but merely a factual observation about a key tenant of our democratic institutions. If the U.S. Constitution can be likened to the “core protocol algorithm” dictating the manner in which our collective network operates, this is a clear attack on one of the most vital rules of the protocol. How can we so readily dilute our core principals?

First, network effects are powerful. The ability of the internet companies to sustain and grow off individual resources, with extremely low detachment rates, cannot be underestimated.

How did this come to be? A failure in timing. As is often the case with disruptive technology, its usage preceded an appropriate infrastructure to handle it. Unfortunately, the Byzantine Generals Problem was not solved before the advent of the internet. Consequently, we have been suffering the consequences that a lack of enforceable property rights leads to in a digital world. A winner takes all society.

This is what the internet got wrong. You didn’t own anything. No one had any stake on the internet. Instead, value has been extracted by those who figured out ways to own the on-ramps and access points to the internet instead.

This group has become the “landlord class” of the internet, and the vast majority of value proffered by the internet and its myriad innovations of social communication has been funneled through this layer. The consequence, of course, has been more inequality, more surveillance and control, and more concentration of power. Further, we’ve witnessed a trend toward a reduction of quality of information. There is a diffusion of responsibility that engulfs the internet when ownership is so opaque and ephemeral. We are incentivized to create more noise than signal because when no one owns the land, there is no incentive to be a steward of that land to ensure its long-term sustainability, utility and productivity. Instead, the incentives align so as to be solely transactional. The more information one can manage, control and recapitulate, the more one can develop network effects and externalize the social and economic cost of a system that produces excessive noise and underproduces enough structured signals that could offer synergistic benefits across societal planes. That cost is shared by all of society. It’s a tragedy of the commons. All because the internet couldn’t address digital property rights.

The second issue here is that network effects also impact passive investing. Most passive vehicles are ETFs, that are indexed and weighted by market capitalization. The bigger you are, the more capital you attract. Size matters, aptitude and productivity do not. This takes us back to the Pareto principle and the 80/20 rule, setting the stage for increasingly non-linear distributions of capital. And in a world where access to low-cost capital is a massive competitive advantage, we end up with an obvious outcome. The big continually get bigger, and the small get only smaller. Or worse, the upstart disruptors may never have a chance, and we would never even know what could have been.

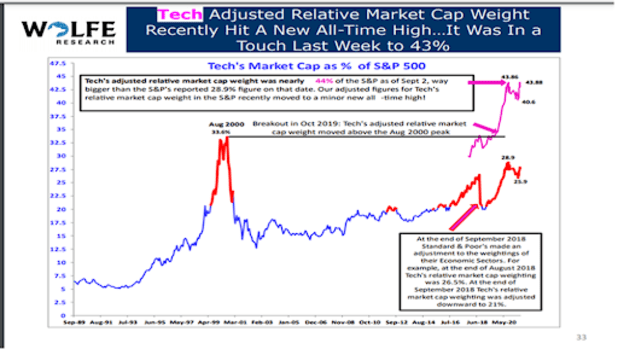

That brings us to the present, where just six behemoths have a near majority control of the entire equity market. Most investors do not blink at this statistic any longer. Professional investors have been numbed to such lopsidedness. However, imagine if such inequality persisted within the domain of political parties? In democratic institutions? In your childrens’ classrooms? But the real question we need to start seriously and honestly asking ourselves is this:

If the below chart only becomes even more extreme in its weighting distribution, and if our collective wealth is increasingly tied to the index it represents, what will our incentives be as the companies involved become even more centralized?

About 45% to 50% of our savings are tied to companies that could be actively censoring us, and indirectly eroding the very principles of the system that allowed them to prosper. This share of our savings will only grow further. Will we object? I certainly hope so. But so far, there is little evidence to support that aspiration. Unfortunately, passive investing, alongside a mass investor class, is likely to only help internet platforms and capital markets centralize further.

Major stock indices are mainly just six names now: Apple, Amazon, Facebook, Google, Microsoft and Nvidia, totaling 42% of the equity market.

Block Five: All Roads Lead To Zero

What happens when zero volatility is the new equilibrium?

After our modest digression into passive investing, let us now return to the last block in our chain. The final and most deadly flaw in the chain reaction socializing financial assets relates to volatility and the cost of capital. Mathematically speaking, publicly-administered financial markets that demand continuous appreciation, distributed broadly and without diversification, will require volatility to trend toward zero over time.

A simple law in financial markets, when assessing an asset’s volatility (as measured by its standard deviation of returns over a given period), is that the more vulnerable to uncertainty an asset is, the less it can absorb volatility. This is why, for example, equity investors are generally willing to pay lower valuation multiples for cyclical or economically-sensitive sectors relative to secular growth or defensive industries. These types of companies are more vulnerable to unforeseen events. When our financial markets are a tool of policy rather than an expression of free market capital allocation, we eventually become incapable of withstanding any uncertainty. And manipulation to affect policy outcomes would be the only way to ensure uncertainty’s suppression. If successfully orchestrated, volatility must eventually collapse toward a zero bound to accommodate this.

As our centralized debt trap expands in circumference, the risk-free rate must also trend toward zero, as has been the case over the past 40 years. Over time, the consequence of this could even be the elimination of the need for a private sector.

This last section is essential to our thesis, as it is the bridge that transports us from the current transitional sandwich era where we find ourselves juxtaposed between centralization and decentralization. This is the last stop on this transitional train as we push relentlessly down the path toward a more authoritarian world order. Given its level of importance in our story, it requires some more detailed explanation.

Centralization As A Black Hole: The Volatility Singularity

What is the volatility singularity? Previously, we have established the logical chain of cascading events that are required in our world’s existing model.

Debt must go up, so stocks must go up. Thus, rates must go down, so volatility must go down. When this happens debt will logically go up, leveraging the system even more, so stocks must go up to prevent collapse and inflate the debt bubble with a greater equity cushion... (stop for breath)… So, rates must go down again until zero, so volatility must go down until zero.

Volatility collides with zero. Everything goes to infinity. Yippie! The transcendent state where the difference between nothing and everything gets very fuzzy and rather philosophically confusing. Just as observed in the case of black holes, where physics starts to behave mysteriously and spooky as one approaches the event horizon, so too do economies. Things start to get pretty eerie as we approach the zero point event horizon in volatility.

Thinking about the problem in the following simplified manner may be helpful:

Anything divided by zero equals infinity. Financial assets returns are a function of volatility. A common formula used to calculate risk-adjusted returns is called the Sharpe ratio, which is an asset’s return during a given period, minus a market risk-free rate, divided by the investment’s standard deviation of returns. If volatility is, for all intents and purposes, equal to zero, so too is its standard deviation. Thus, we end up in a confounding situation in which excess returns are divided by nothing, and therefore magically become, well… everything.

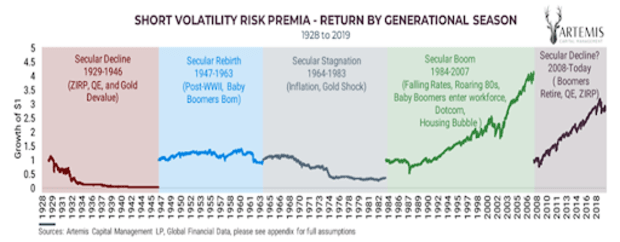

As macro volatility fund manager Christopher Cole excellently laid out in a 2020 piece titled “The Allegory Of the Hawk And The Serpent,” an investment strategy designed to short volatility, or benefit when it decreases, experienced temporally anomalous returns since the early 1980s, right when the financialization of Wall Street took off exponentially, and right as Alan Greenspan et al. began a campaign of moral hazard, at a time known as “The Greenspan Put.”

The stock market and nearly all financial assets in aggregate then become just a mere proxy for this “short volatility” expression.

An Endangered Golden Goose

Cole, like many others, believes this period of declining volatility is mean reverting and must therefore repeal its nearly 40-year journey. While certainly possible over a cyclical short term time horizon given the magnitude of the move, a spike in volatility is unlikely to be palatable for any sustained period. The reason, as you might have guessed, is because of the deterministic nature of acceptable outcomes laid out above. The violence to the system that a spike in volatility would require would eviscerate so much wealth, so many debt obligations, that the policy response would be equally violent. Such a response is all but guaranteed because the crisis would be existential for those in power.

This outcome becomes more assured each day that goes by with greater reliance on financial assets to lift us into the future, each day that a citizen puts their first dollar of savings into such a system, and each day that another dollar is diverted away from new capital expenditure in favor of being recycled instead back into the existing sinkhole.

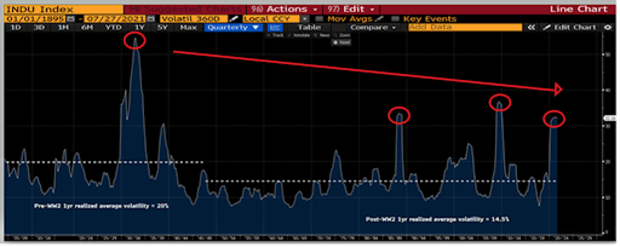

Below is a graph of the realized one-year volatility in the Dow Jones Industrial Index going all the way back to 1895. The pre-WWII average of this proxy for stock market volatility was about 20%, witnessing only one to two “black swan” spikes during a 50-year span. Meanwhile, the post-WWII average has been closer to 14.5%, with three black swan events observed only within a 30-year period!

This graph gives us two important pieces of information:

- Volatility is trending lower over time. A move from 20% to 14.5% may not sound significant, but this is a nearly 30% decline in average volatility. The positive effect of such a shift has on underlying asset prices cannot be overstated.

- A system of declining volatility has come at the heavy cost of greater susceptibility to bouts of near-disastrous black swan events, external and internal shocks. And these events are not capable of being permitted to clear the imbalances that caused them, to self correct, as the system would break before such catharsis could be attained. Instead, each successive crisis forces policymakers to intervene at much lower levels of volatility than in the pre-WWII era. This of course fuels greater abdication of responsibility, which fuels the next crisis as we rinse and repeat, racing toward zero.

Centralization Is A Fabergé Egg: Systems Which Require Stability And Efficiency Are Always Extremely Fragile

I recently came across a white paper authored by Ben Inker and Jeremy Grantham, famed hedge fund investors at GMO. They conducted a data mining project and looked at the prior periods of frothy financial markets like the 1999 to 2000 period, and similar historic periods of strong performance and excess returns. They were surprised to find that it wasn't earnings growth, the level of real interest rates, or even GDP growth that mattered during such periods of excess and euphoria.

Instead, they found three consistent variables that were always part of the equation:

- Atypically high profitability for one or some segments of the economy (this is finance speak for maximal efficiency rather than maximal productivity)

- The stability of GDP (as a proxy for overall economic activity)

- The stability of the rate of inflation

In short, markets care not about actual levels of growth, inflation and profits. Predictability is what matters. A financialized system and a mass investor class requires stability and loathes uncertainty. Said differently, our system of monetary inflation rewards monopoly formation, values efficiency over productivity, and requires reduced volatility to sustain itself.

Given that volatility is a natural phenomenon of any free system, suppressing it requires external and artificial forces. It requires a central authority to manage the system and to solve for low volatility. Our central bank policy of monetizing moral hazard is evidence of this. Moral hazard from this prism is simply a function that solves for low volatility, at all costs. And there are a lot of costs.

The Difference Between A Medicine And A Poison Often Comes Down To Dosage

While the importance of gains in efficiency are indeed a requisite aspect of technological progress as well as a tremendous generator of wealth for those providing such efficiency gains, there is always a trade off. A great example of this is the Bitcoin block size war of 2017, as well as the many utility protocols proliferating the crypto universe, optimizing for network throughput at the cost of much weaker decentralization. The irony is that the many use cases of blockchains become completely obsoleted without decentralization. Efficiency is great. It’s exciting. It often is associated with innovation. To a point.

Where is this point?

Any marginal gain in efficiency requires a marginal loss of resilience. Given that resilience is vague and incandescent, a decline can seem harmless until it suddenly breaks completely. This means that the relationship between efficiency and resilience is non-linear. There is always a point on the curve where the benefit of efficiency gains become precipitously overwhelmed by the cumulative trade-offs.

Ok, fine. Let’s agree that the financial system is in fact becoming more fragile. What does this have to do with centralization of power? Shouldn’t a fragile system lead to the dissolution of power?

Short answer? No.

Less short answer? A centralizing power depends on vulnerability to validate its own existence. As the costs of centralization mount, is becomes existentially vital for an authority to lay claim on the sole ability to medicate the very ailments it fabricates, so as to traverse unstable times unscathed. Fragility maintains power. Power thrives on fragility.

Efficiency Is A Great Barometer Of Where We Are In The Macro Cycle

Why? Efficiency naturally peaks at the end of a regime. By the end of the regime, everyone assumes the cycle to be permanent because no one remembers a different world. We succumb to recency bias, forget history, and inadequately discount the inevitability of change.

Efficiency, fundamentally, is a way of optimizing processes or work to a specific environment. By the end of a regime’s lifespan, an environment’s self-selected economic participants have naturally maxed out adaptations to that one environment, having gone “all in” on its defining characteristics.

Thus, like a grain of sand placed on a growing sandpile, all that is needed is just one inopportune shift and the whole system cascades down with surprising fragility. A meteor hits, and we are cold-blooded, energy-consuming goliaths. Good luck with that!

We’ve of course seen this story time and time again throughout history, both at biological and evolutionary scales when diversity is overcome by uniform specialization, and throughout the annals of human history. This is one explanation as to why empires always eventually fall. Their successes eventually become their weaknesses. Efficiency helps fuel dominance in a world that values power as a function of resources, but it leads to dangerous deficits in resiliency that inevitably make them easy to destroy. This is also why empires are often built over long periods of gradual ascent, but often fall precipitously. Non-linearity.

Thus, somewhat counterintuitively perhaps, periods of maximal efficiency will precede periods of instability and upheaval.

An Obituary For The Private Sector

Now, let us return to volatility.

As the boulder of zero volatility and a fully-managed economy slides precipitously toward its Newtonian fate, there will slowly materialize some incredibly powerful implications for the structure of private property rights. This is because zero volatility and a required real risk-free interest rate held at zero or negative levels will logically push the aggregate cost of capital to extremes.

When there is no risk of material loss for capital, there becomes no discrimination as to how to invest it. The decision-making process becomes tied much more to government policy goals, cronyism and bribery, and other characteristics very similar to those of communist systems of governance. The corporation and the entrepreneur lose their utility in this world.

The birth of the modern corporation can be traced back at least to Adam Smith’s 1776 classic, “Wealth Of Nations,” interestingly published the same year that colonists here in America sought independence.

In this work, he lashed out at the “business association,” his era’s version of the state-owned companies, or the precursor of the “military-industrial” complex, or in China’s case the Sovereign-Owned Enterprise (SOE). These were institutions like the British and Dutch East India companies in Smith’s time.

He argued against monopolist business practices, which in turn paved the way for the legal autonomy of business outside the direct control of the government. As far back as 1844, corporations began earning the status of “personhood,” eventually granting them 14th Amendment rights in 1886. This paved the way for the evolution of corporate oversight toward the domain of the court system and not that of the executive and legislative branches.

The point here is that while we sometimes think of corporations as gatekeepers, monopolists, greedy beneficiaries of consumerism, debt and inflationary growth, these adjectives describe their failures within our current system, not their original purpose. The corporation was originally designed to bestow greater power to the entrepreneur and decentralize power away from the state.

By providing legal protections like limited liability, the corporate structure allowed for individuals to combine resources without unmanageable personal risk, which in turn allowed for the competitive acquisition of capital for investment. So, when the cost of capital and the risk of capital become immaterial, the existential purpose for the corporation becomes difficult to justify. And so the economy centralizes further with the erosion of one more source of decentralization.

What is so exciting about Bitcoin within this context is that it replaces the vacuum created from an impotent corporate private market structure with something much more decentralized and much better suited for the evolving digital information economy. It helps an increasingly interconnected economy divide labor beyond its current stalemate.

Bitcoin is a medium of specialization. Corporations were invented to be a specializing spoke of private capital, allowing for greater and more scalable division of labor. Unfortunately, in a world where the digital realm is becoming the majority sphere of economic activity, where individual property rights had not been assured prior to Bitcoin, the corporation instead has more often become a rent seeker, a bottleneck for competition, and a gatekeeper of digital property. This has had the perverse effect of decreasing our collective ability to specialize. Bitcoin solves this problem.

However, I am getting ahead of myself. We will get into this exciting potential in greater detail in part two of this series.

A Dangerous Cocktail: Why The Pareto Principle Matters

As the world becomes more interconnected, relationships become more “Paretian,” and less “normal,” or mean reverting. This is because the Pareto principle has shown empirically that complex systems often demonstrate extremely asymmetrical distributions of effect. Effects that only magnify as the system grows larger.

Prior to the interconnectedness driven by technologies and the scalability of digital networks, such Pareto effects were only discernible at ultra-large scales or where the complexity of the system was much larger than witnessed in everyday life, in fields such as macroeconomics, astronomy, geology, ecology and theoretical physics. But over time it is being appreciated just how pervasive this Pareto dynamic truly is.

In the business world, it has been shown that roughly 20% of customers often produce 80% of a company’s revenue. Eighty percent of a company’s output, likewise, is often generated by 20% of its employees. The pattern is found in many random systems. Eighty percent of highway accidents occur at 20% of the path traveled (near home), 80% of the cost of building is spent on 20% of the structure, and 20% of the world population is responsible for 80% of the pollution. The list could go on. But this simplified 80/20 rule actually understates the impact, as it is simply an approximate guide, the map rather than the road itself.

In fact, this 80/20 ratio can often turn into 99.9999/.0001 quite easily. Take a simple example where the square root of the total nodes in a given network is the number of nodes that are deemed to have the most measurable impact on that network. If we start with 10 nodes, we have about three nodes fulfilling that role, or about 30%. If the network grows to 500 nodes, we get about 22 nodes, or less than 5% of the network. If we end up with 500,000 nodes on the network, the figure would be about 707 nodes providing that impact, or a stunningly small fraction of 0.1%. Non-uniformity scales exquisitely.

As we begin to see, the Pareto principle is powerful in large systems, and is so important today as the world interconnects exponentially and in increasingly fractal patterns. The bigger the network, the more extreme the variance. Decentralization is a natural outcome of network building, especially if allowed to flourish without interference or external exploitation. Therefore, it is a logical conclusion as a general principle that decentralization increases variance and begins to break down previous patterns of mean reversion that are so characteristic of normal probability distributions.

Conversely, centralization craves more uniformity. Otherwise, there become too many outliers in the herd to corral, and the system becomes unmanageable. As networks proliferate, governments increasingly are driven existentially to ramp up the use of power and coercion against this natural force.

Not only is the world experiencing greater dispersion of outcomes, it is also changing at an increasingly faster pace. Raw data is pouring torrentially down upon us, overwhelming our neural capacity more each day. We are confused, overwhelmed and looking for anchors, answers, and authority.

“Black swan” or “tail risk” events, by definition, are not predictable by any model. Otherwise, they would not be black swans. Models often give us a false sense of stability, understanding, and confidence. The renowned behavioral economist Daniel Kanneman has shown that even when we are given statistical predictions that we know to be spurious, we embarrassingly cannot help but feel assured and make more risky decisions based on such irrelevant data.

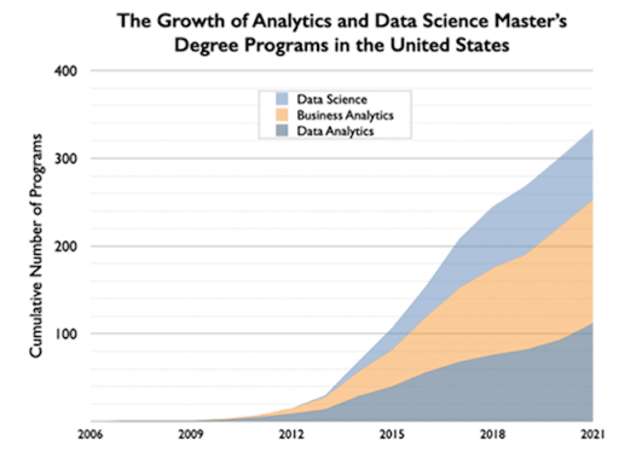

Nonetheless, the pace of change and data dumping has inspired us to overly romanticize and revere data accumulation, prediction, and data modeling techniques. We even have new professions that have popped up to deal with such issues, often aptly referred to as data “scientists.” Most major universities over the past decade have added degree programs for data science and it is now one the fastest-growing programs in academia.

Now, let us more holistically recapitulate the situation described above. The cacophony of noise is getting ever louder, and meanwhile, our ability to filter this data to uncover the important signals hiding within has not improved at all.

We have developed technological tools that can filter the raw data and improve its informational extractability. However, these improvements are limited solely to endeavors that we are comfortable deferring to computers to manage for us. In all activities where humans still require involvement or apprehension, we are completely outmatched. On top of this, technology can be a tool, but it can also be a weapon. For every search, storage and AI tool that has helped to unbundle the noise into some semblance of a signal, there are other software tools that re-bundle the signal once again back into noise. Particularly social media, mainstream media, political propaganda and social science professions that overconfidently apply the newfound data abundance.

Taking all of these themes together, we have rampant technological shifts, overwhelming data propagation, and overconfident and confused human actors trying to adapt to these self-inflicted changes to achieve the unattainable: control. This means an increasing risk of the black swan events we so fiercely aim to circumvent. Less predictability, and more hubris as to our collective capacity to pattern-recognize and avoid those rare and historically pivotal events. This is a very dangerous cocktail.

An Homage To Endurance, Tenacity And Immutability

“I think much more likely is an even worse alternative: government will not cease inflating, but will, as it has been doing, try to suppress the open effects of this inflation. It will be driven by continual inflation into price controls, into increasing direction of the whole economic system. It is therefore now not merely a question of giving us better money, under which the market system will function infinitely better than it has ever done before… but of warding off the gradual decline into a totalitarian, planned system, which will, at least in this country, not come because anybody wants to introduce it, but will come step by step in an effort to suppress the effects of the inflation which is going on.” –Friedrich A. Hayek, "The Collective Works of F.A. Hayek," "Toward a Free Market Monetary System."

Endurance, tenacity and immutability. While these attributes may sound too passive or unsubstantial to have value in our “move fast and break things” world, they are the exact traits required to survive the fragility of a system dashing feverishly towards instability.

Antifragility, an idea popularized in the 2012 book “Antifragile” by Nassim Taleb, describes systems or phenomena that gain strength from disorder. This book, part of a larger work focused on philosophical, statistical, and economic misconceptions relating to systemic risk, uncertainty, and randomness, has become part of the larger canon of Bitcoiner manifestos. This is despite Taleb’s recent baffling divorce from the community, which while a tad perplexing, should not detract from some of his work’s takeaways.

Bitcoiners have latched onto the themes of “Antifragile” as a framework to help elucidate some of Bitcoin’s game theory. How is it that there is no silver bullet that kills Bitcoin, there is no competitor that can magically overtake it, there is no government that can shut it down, and there is no central authority that can censor or confiscate it?

But the message does not stop there. Most important to the thesis of antifragility, each attack vector and shock to the system in fact causes Bitcoin to become stronger.

As Taleb writes:

“Some things benefit from shocks; they thrive and grow when exposed to volatility, randomness, disorder, and stressors and love adventure, risk, and uncertainty. Yet, in spite of the ubiquity of the phenomenon, there is no word for the exact opposite of fragile. Let us call it antifragile. Antifragility is beyond resilience or robustness. The resilient resists shocks and stays the same; the antifragile gets better. This property is behind everything that has changed with time: evolution, culture, ideas, revolutions, political systems, technological innovation, cultural and economic success, corporate survival, good recipes (say, chicken soup or steak tartare with a drop of cognac), the rise of cities, cultures, legal systems, equatorial forests, bacterial resistance … even our own existence as a species on this planet. And antifragility determines the boundary between what is living and organic (or complex), say, the human body, and what is inert, say, a physical object like the stapler on your desk... The antifragile loves randomness and uncertainty, which also means — crucially — a love of errors, a certain class of errors.”

We have seen firsthand how the market can reward an asset that exhibits antifragility. Astute macro investor Louis Gavkal has wisely observed that this is how the U.S. treasury market has evolved.

Today, investors have institutionalized portfolio management, packaged into strategies like 60/40 asset allocations (bonds/stocks), and slightly more volatility-adjusted strategies such as risk parity. However, this love affair with the treasury market as a diversification tool has not always been the case, especially from the perspective of global investors. In fact, treasuries may be losing this status. The godfather of risk parity, Ray Dalio himself, just recently confirmed the view that he would rather own bitcoin than bonds.

What has historically given treasuries their stature of primacy for so many years was the dollar’s reserve currency role. A feat attained through war, geopolitical victories, petrodollar arrangements, and the trade-offs of increasing consumerism and domestic debt accumulation in the U.S. to supply dollars abroad. All punctuated by a parallel hyper-financialization of our economy, with regulatory incentives to own treasuries and a global system addicted to dollar-based leverage and short of adequate collateral.

This collateral shortage has become particularly acute after quantitative easing has been significantly reducing the public supply of treasuries since 2009. All of these factors have helped create a treasury market monster with very resilient network effects for the U.S. dollar. Resilient to deleveraging elsewhere, resilient to market volatility, resilient to dollar shortages, and even resilient to cyclical inflation.

The treasury market is a massive battleship that has been chugging along full steam in one direction for many years. However, this ship is now altering its course. And this process is ever so slowly chipping away at those network effects. As the U.S. dollar necessarily loses some strength as a reserve money, the system will either need to deleverage or find a new source of collateral, a new antifragile asset.

One way to think of the U.S. treasury market’s ability to maintain buyers and holders despite real interest rates, at least at negative 1% (depending on your gauge of inflation), is that this market has become a weigh station, a storage space for dollar-denominated assets, intended to balance existing portfolios of dollar-denominated equity, real estate and corporate debt holdings, as a reserve account that incentivizes participants to remain within the bounds of the existing USD ecosystem.

The Eurodollar system, U.S. dollars banked or held outside of the U.S. banking system, evolved to help accomplish this goal more efficiently at the global level.

The Eurodollar market size has exploded as the U.S. economy began to financialize in earnest: First in the early 1980s and then again in the 1990s and post-dot-com burst.

The start of this in the early 1980s coincided with the start of a 40-year bull market in U.S. treasuries:

Such a concept of captively on-ramped capital is actually very similar to the stablecoin market in the Bitcoin and cryptocurrency ecosystems.

Unfortunately, for the U.S. dollar fiat ecosystem, there are signs of deterioration within its network effect. Foreign users are balking.

A Poetic Phrase: Bitcoin Is A “Deep Structure”

“In a Paretian world, surface events can become a distraction, diverting attention from the deep structures molding these surface events. Surfaces are extraordinarily complex and rapidly evolving while the deep structures display more simplicity and stability. These deep structures are profoundly historical in nature — they evolve through positive feedback loops and path dependence. Snapshots become misleading and understanding requires a dynamic view of the landscape.” –John Hagel

We live in a world where things are intentionally made to fall apart. Quantity and popularity are valued above quality and depth. The news cycle is a meager 24 hours. Medical and health problems are addressed ex post facto with newly-invented medications and treatments, rather than by way of lifestyle changes and preventative measures.

Products are meant to become obsolete. Buildings are designed to last 20 years rather than 200. Tweets share ephemeral memes instead of lasting ideas, investments are made for instant return potential rather than lasting productive impact. And interest rates have collapsed to near zero, allowing us the mathematical permission to discount the future so that it is indistinguishable from the present.

We have lost our ability to think long term. We have no appreciation for durability over time. Therefore, we do not particularly value persistence because its main attribute is indeed durability over time.

Taking this a step further, if we do not place any material value on resilience, how could we value antifragility at the societal level? This is because antifragility is simply resilience in the form of a productive asset. By this I mean something that is durable, but also something that improves over time. It is no wonder then, that even Bitcoiners may be undervaluing antifragility.

This irony is further extended by the fact that just at the time when civilization least values such a high-powered form of durability and productivity happens to also be when these attributes are most desperately needed.

Antifragility is an embrace of volatility.

Volatility is the mathematical expression of what biologists and evolutionary scientists might call a “stressor.” Biological organisms crave stasis. Volatility, on the other hand, is a natural characteristic of all complex systems. This is because the greater the number of variables, the greater the number of possible outcomes. Stressors lead to adaptation and growth, which leads to survival, which builds resilience, which lays the foundation for more resilience and growth.

It is a positive compound growth formula because the more resilient we get, the more volatility we can swallow, without choking on it. As implied above, an increase in volatility can be thought of in this context as just a greater range of circumstances. But this can come from two sides, like a matrix of potential outcomes.

On one axis, you have a quantity and variety of stressors, but on the other you also have a quantity and variety of reactions, responses and results. In a decentralized system, both axes expand over time, generating an exponential function as two growing variables are multiplied by one another. When systems lack a centralized gatekeeper, more stressors are allowed to propagate. Likewise, there is greater diversity and heterogeneity of participants that can react uniquely to these stressors.

When this happens, life happens. Creativity manifests. Innovation blossoms. Individuals are at their best. Societies are at their best. We experience more possibilities and improve our probabilistic odds of discovering something of immense value, and we do so exponentially.

A principle: Bitcoin, like all of nature’s evolutionary survivors, is forged of persistence. And persistence is forged from savings.

As Albert Einstein is (perhaps apocryphally) credited with saying: “The most powerful force in the universe is compound interest.”

Compound interest is one of the most impressive growth formulas experienced in the natural and economic worlds, and its most efficient avenue for success is antifragility.

Regardless of whether Einstein indeed ever uttered these words, the important takeaway here is that of Pareto distribution curves in exponential growth. The reason the “powerful force” of compounding growth is driven by antifragility is because it is raised by the exponent of time itself.

Survive like our palm tree and you get to keep compounding. As long as the other variables in the equation do not change materially, time will do the heavy lifting. This speaks to an important point on the importance of resilience when it comes to financial assets, as consistency through time is what leads to such tremendous abundance.

“What’s the most powerful force in the universe? Compound interest. It builds on itself. Over time, a small amount of money becomes a large amount of money. Persistence is similar. A little bit improves performance, which encourages greater persistence, which improves persistence even more. And on and on it goes.” –Daniel H. Pink, “The Adventures Of Johnny Bunko”

In a previous article, I cited the above quote referring to what I perceived to be bitcoin’s ability to compound a type of accrued interest over time relative to fiat benchmarks. My argument laid out how something like hyperbitcoinization could result from this compounding power law function, and therefore see its growth curve actually accelerate in the future, rather than level off in an asymptotic “s-curve” shape — something that may be underappreciated even by the most ardent bulls.

Interest earned, in a free market, is the equilibrium price required to balance one’s time preference of consumption relative to savings. One of the oldest axioms of economics, Say’s law, observes that we are always both consumers and producers. Even as consumers, we are producers of specialized labor to accumulate resources to be used to consume at some future point.

Money, a human social technology of value and communication, is perhaps one of the few practical instances we can witness of a limitless power law function, as it stores labor over time. In a power law equation where time itself is the variable to which the function is raised, this creates a powerful compounding effect. That is, as long as the calculated value can persist over time.

An absolutely scarce money accrues its interest as the residual incremental productivity gained from marginal output. New productive labor can only scale if work can be continually divided and specialized. Such scaling, in turn, can only occur if there is adequate savings of excess production.

Excess saving leads to specialization, allowing for innovation and productivity gain, in turn generating additional savings. If this equation is disrupted then this virtuous progression collapses.

What does all the above have to do with antifragility and persistence? It points to a fatal flaw in an increasingly centrally-controlled fiat money system.

It is a matter of first principles. There simply cannot persist a functional money in a society whose main product is credit. Things can start fine but the nature of credit is similar to a drug, especially when the transmission of credit is centralized by a trusted rule-making body. Such a system encourages at least two horribly problematic outcomes: